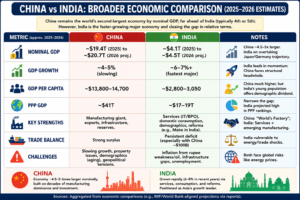

China remains the world’s second-largest economy with a nominal GDP projected above $20 trillion by 2026, nearly five times larger than India.

BY PC Bureau

May 25, 2026: China’s yuan (CNY) has reached a three-year high against the US dollar, with USD/CNY trading around 6.78–6.80 recently (e.g., 6.795 on May 24–25, 2026). This represents a notable appreciation, with the yuan strengthening by over 5% in the past year by some measures.

The rise is linked to hopes of a deal ending the Iran conflict and the partial reopening of the Strait of Hormuz, a critical chokepoint for global oil and LNG supplies. Even a marginal recovery in shipping would ease energy pressures on China, a major importer. As one Chinese bank trader noted to Reuters: “It might be hard to fully restore cross-strait shipping for the time being, but even a marginal recovery would be positive for financial markets.”

In contrast, the Indian rupee (INR) has hit record lows, trading around 96.50 INR per USD in May 2026 recently, with all-time lows reported around 96+). This makes it one of Asia’s weakest-performing major currencies amid foreign outflows, elevated crude oil prices due to Middle East tensions, and a strong dollar.

Key drivers of rupee weakness include India’s heavy reliance on oil imports, vulnerability to Hormuz disruptions, widening trade deficits, and capital outflows. The rupee has depreciated significantly during 2026, exacerbating import costs while potentially aiding exporters.

READ: Assam Introduces Uniform Civil Code Bill in Assembly

Implications: A stronger yuan supports China’s import purchasing power and helps control inflation from energy costs. A weaker rupee raises India’s import bill — especially for oil — and inflation risks, but boosts competitiveness in exports and services.

Broader Economic Comparison: China vs. India (2025–2026 Estimates)

Key Strengths (China):

Manufacturing giant, exports, infrastructure, reserves Services (IT/BPO), domestic consumption, demographics, reforms such as “Make in India” China is the “world’s factory”; India is services-led with emerging manufacturing strength.

Three things happened to the dollar this month:

🇨🇳 Yuan hit 3-year high (6.79)

🇯🇵 Yen at 4-year inflation low, BOJ shifts dovish

💵 DXY testing 2026 lows (~99)This is what the start of a softer-dollar cycle looks like.

Historically: when DXY falls 10%, gold and emerging market… pic.twitter.com/430tURN1Wr— AInvest Wire (@Ainvest_Wire) May 25, 2026

Trade Balance Strong surplus Persistent deficit (especially with China, around $100B) India remains vulnerable to energy and trade shocks.

Challenges Slowing growth, property crisis, ageing population, geopolitical tensions Inflation from rupee weakness and oil prices, infrastructure gaps, unemployment Both economies face risks from global energy volatility.

China’s economy is roughly 4.5–5 times larger in nominal terms, built on decades of manufacturing dominance and infrastructure investment. India has grown rapidly — often at 6–8% annually in recent years — through services, consumption, and policy reforms, positioning it as Asia’s key growth engine for the coming decade. Projections suggest India could sustain growth above 6% into the 2030s, while China’s growth may slow toward 4% or lower.

Impact of Geopolitics and Energy (Iran Conflict & Hormuz)

The ongoing Iran-related conflict has disrupted the Strait of Hormuz, through which roughly 20% of global oil and LNG flows. China imports heavily through the route, with an estimated 36–50% exposure to crude supply via Hormuz. However, stockpiles and diversified suppliers such as Russia help cushion the impact. Hopes of reopening have supported the yuan by easing fears over energy inflation and improving investor sentiment.

India, also heavily dependent on energy imports, faces mounting pressure from higher oil prices and rupee depreciation, which have contributed to the currency’s record lows and strained the current account balance. While both nations would benefit from stabilization in the region, China’s larger reserves and economic scale provide greater resilience.

Outlook

China: Yuan strength signals confidence in economic stabilization. Beijing remains focused on exports, technological self-reliance, and managing slower growth. A stronger yuan may aid economic rebalancing but could pressure exporters.

India: Rupee weakness remains a challenge for imports and inflation, though it could support the “China+1” manufacturing shift and boost services exports. Long-term fundamentals — including demographics and the digital economy — remain strong, while RBI interventions and foreign exchange reserves offer buffers.

Comparative Edge: China retains a decisive advantage in economic size and industrial capacity, while India leads in growth momentum and services. The pace of convergence will depend on India’s manufacturing expansion and China’s ability to navigate structural economic challenges.

This evolving dynamic underscores diverging trajectories: China’s mature but slowing economy versus India’s rising catch-up potential amid global uncertainty. Currency movements reflect immediate geopolitical and energy concerns, while deeper structural factors will shape the long-term economic contest between Asia’s two giants.